Latest Dashboard: Macro and Markets Dashboard: United States (PDF)

Data over the past week has been both terrible and good, as US equity markets had their worst ever start to the year, but the jobs report was positive. Volatility in Chinese equity markets has been largely cited as the cause for the U.S. sell off. The S&P 500 fell nearly six percent during the week (see below). Oil (WTI) fell about three dollars a barrel over the week.

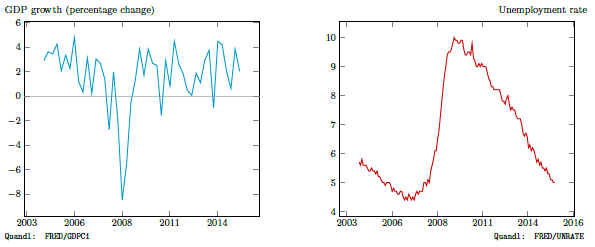

Meanwhile, jobs data showed a slight uptick in the extraordinarily low labor force participation rate, and a stable five percent unemployment rate. These, the jobs increase, and wage figures, are better than what was generally expected.

The trade weighted dollar strengthened, as the dollar strengthened by more than a percent over the British pound and Chinese yuan during the week, and by more than 3.75 percent against the Australian dollar. It now takes more than 1.41 Canadian dollars to buy a U.S. dollar.

The Fed’s H.4 report shows lots of activity as the reverse repo offerings reflect the Fed’s unconventional tools for draining liquidity from markets. Excess reserves of depository corporations have fallen to their lowest level since 2013 (see far below).